The Curriculum

Decoding the matrix.

9.5 hours of on-demand technical video, broken into 29 focused lessons.

Five pillars. No fluff.

We do not teach software

We teach X-ray vision.

Here is the question we get most often: why are you making me calculate an experience mod by hand when I have software that does it for me?

Fair question. Here is the honest answer.

Your rating software is only as good as the data going into it. When there are errors in the data, the software will calculate that error perfectly and hand you a clean-looking output.

When you understand how the primary threshold works, how the D-ratio splits excess from primary losses, and how a single open reserve distorts the ballast value, you stop trusting the output blindly. You start reading the worksheet the way a forensic accountant reads a balance sheet. You can also explain the mod more simply the more completely you understand it. That is X-ray vision. That is what this curriculum builds.

Fast Facts

Course structure

- Format: 9.5 hours of on-demand, highly technical video modules broken into 29 focused lessons.

- Core topics: State-by-state rules, experience rating mechanics, mod math calculations, injury management protocols, and premium audit deconstruction.

- Testing: Final exam requiring you to show your work on actual calculations. Unlimited retakes with targeted, human feedback.

- Depth: Covers the full technical foundation of the CWCA plus advanced material — with retail sales tactics stripped out entirely.

Inside the portal

29 tactical videos, organized into five pillars.

Every module lives inside the WCTP portal. Train on a specific mechanic

during a lunch break, then immediately apply it to the file on your desk.

Pillar

01

The Rulebooks

- Rating Bureau Navigation

How to actually read and apply the NCCI Basic Manual, the Experience Rating Plan Manual, and the Scopes Manual. Not summaries, the actual documents. - Independent Bureaus

NCCI does not govern every state. We pull apart the independent manuals for California, Pennsylvania, Delaware, and New York so you are not caught off guard when a risk crosses state lines. - State Law Mechanics

Using resources like the US Chamber of Commerce Analysis of Workers’ Compensation Laws to walk through the differences in waiting periods, retroactive periods, and specific injury benefit schedules. The rules are not the same everywhere. Assuming they are is expensive.

Pillar

02

Experience Mod Mechanics

- The Valuation Date

The most important day in the experience rating cycle, and the one most professionals miss. Exactly when it happens — 18 months after policy inception — and what it means when an open reserve gets locked into the mod at that snapshot. Potentially serious impact on the mod, frozen in place because nobody was watching the calendar. - The ERA (Experience Rating Adjustment)

In ERA-approved states, keeping a claim medical-only triggers a 70% discount on how that claim hits the mod. Why the decision to open an indemnity payment is one of the most consequential calls in the whole system. - Subrogation Recoveries

A third-party recovery does not just reduce the final settlement. Applied correctly, it revises the current and prior experience mods. We show you the mechanics of how that works and why it is critical to get it right. - Ownership and Combinability

The “common majority ownership” rule catches people by surprise. We show you exactly when entities must be combined, what triggers the requirement, and what happens if an ERM-14 never gets filed. - Cancel Rewrites

Changing a policy effective date is not a clean swap. It alters the Experience Rating Period and dictates which policies drop off the mod and when. We walk through the exact mechanics so you are not blindsided by the downstream impact.

Pillar

03

Mod Math — State by State

- NCCI Split Rating

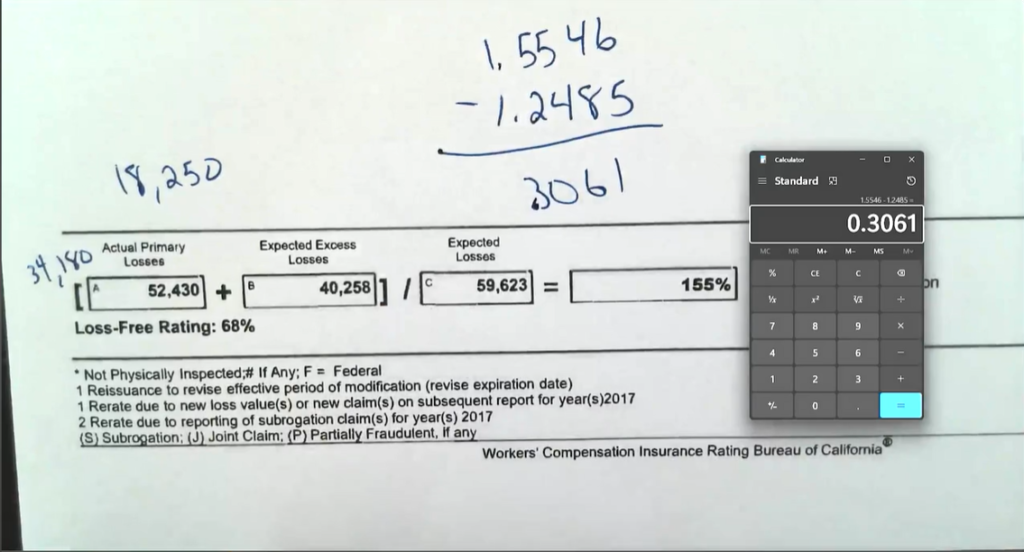

Expected loss rates, D-ratios, actual primary losses, and the ballast value. We walk through each component and show you how they interact. - California Rules

The WCIRB does not operate like the NCCI. The California primary threshold and why the bureau removes the first $250 from every claim before it enters the mod calculation. That rule surprises a lot of professionals who work primarily in NCCI states. - Pennsylvania and Delaware

The PCRB and DCRB use a three-digit classification system. Limit charges and credibility factors so you know what you are looking at when a Pennsylvania risk crosses your desk. - New York Rules

The NYCIRB uses sliding split points and imposes maximum mod caps that vary based on claim count. We walk through both so New York never catches you flat-footed.

Pulling apart the NCCI Scopes Manual

Mod math worked by hand

Pillar

04

Injury Management Mechanics

- The Hiring Process

Many injury problems start before the employee walks onto the job site. You will learn how a Conditional Offer of Employment, post-offer, pre-placement medical exam, and an ADA-compliant functional job description create a legal, documented baseline for physical capability. - Recovery at Work

The most common excuse for skipping light duty is having nothing for the employee to do. How a “Job Bank” eliminates that excuse and keeps indemnity claims off the mod. - Nurse Triage

A minor injury that goes to the emergency room becomes an expensive claim fast. The financial impact of 24/7 telehealth triage and why catching those injuries early is one of the highest-leverage moves in the system.

Pillar

05

The Premium Audit

- Classifications

Standard Exceptions like Clerical (8810) and Outside Sales (8742) get misapplied constantly. The Executive Supervisor (5606) code is one of the most misunderstood classifications in the entire system. We walk through the rules and the common mistakes. We also dig deep into how classifications are written, how they can be applied and how they can’t, and how to make sure that every business you work with is properly classified. - Uninsured Subcontractors

The rules for charging uninsured sub payroll are specific. We dig into the fine points of the rules so that the insurance company gets exactly what they are owed. - Excluded Remuneration

There is money in every payroll that is exempt from premium — overtime premium, severance, specific employer-provided perks, per diems. Most employers are paying premium on money that should never have been included. The exact manual rules for each exclusion.